3 Areas Of Intrigue: Another Fund Data Site, Social Financial Literacy, Pace of Social Finance

/ TweetChicago’s weather has been unsettled (is it or is it not going to rain?), the Chicago Blackhawks have yet to truly assert their superiority in the Stanley Cup Final, and more business meetings/calls have been cancelled in the last few days than have happened. Things are not quite coming together this week.

And so it’s no surprise that I couldn’t close on one of three ideas that caught my attention—what follows is a bit on all three.

New Insights On Fund Distribution

On Tuesday, BrightScope launched Fund Pages, promising to deliver individual investors and financial professionals “deep [data] insights which were previously expensive or hard to find.”

As a quick refresher, BrightScope is “a financial information and technology company that brings transparency to opaque markets.” The firm got its start providing retirement plan ratings and analytics and extended the business a few years ago by building a directory of financial advisors. It’s not much of a leap from its previous work to see it diversify now into mutual fund and exchange-traded fund (ETF) data display that includes a fund scorecard and trended analysis.

According to the Website, the firm obtains its data from both publicly available and private sources, including regulatory filings from the Securities and Exchange Commission and Lipper. A rather prominent note on the fund pages encourages asset managers to make contact about "streamlining" your fund data feed directly onto the platform.

It seems like an uphill climb for BrightScope to take on other fund data sites, Morningstar among the most prominent, but I wish them well. Update: I didn't take it upon myself to compare the product data offerings but some RIABiz coverage published after this post addresses that.

Here’s what’s new from my perspective.

The offer to connect investors with advisors

Fund companies largely rely on advisors to introduce their funds to investors. But BrightScope thinks it could work the other way around. Investor awareness of a fund could prompt a call to an advisor.

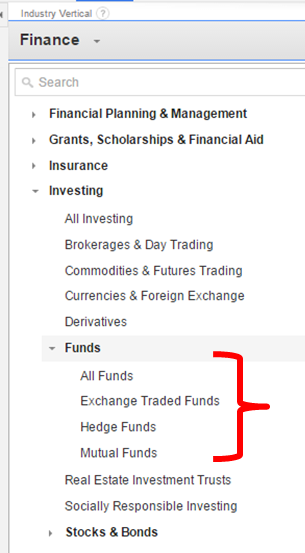

For example, this screenshot shows the three advisors displayed on the Vanguard Total Stock Market Index Fund (Admiral shares) profile.

Clicking on one of the advisors goes to an advisor profile page where there's a contact form. The page also includes a list of the funds the advisors uses.

That’s different and so interesting. It closes a loop in a way that hasn't been done before.

Comparisons of fund company Websites to other product manufacturers’ sites have never quite held up because there’s been something missing: Where and how to buy the product. Every other manufacturer offers product availability information for its retail visitors.

Sure, some old-school firms still conclude all content with the suggestion that investors talk to their financial advisor. But this feature goes much further: Like a fund? Here’s who sells it.

Unlike most of the data on the pages, Advisors Using This Fund information will not be extracted from BrightScope’s database, it will be self-reported by advisors registered in the system and the names displayed in what looks like alphabetical order.

My guess? Adoption will be spotty unless BrightScope finds a way to share success stories (leads) with advisors.

The display of wholesaler information

According to the blog post, registered advisor users will automatically see the wholesaler for the fund they are viewing, and they can email the wholesaler directly through the fund pages.

There’s even more information on that in this MFWire post including a surprising quote from Ryan Alfred, BrightScope co-founder, president and chief operating officer, that “we want to make it easier for advisors to connect with wholesalers.”

Surely, that’s something on which asset managers and BrightScope agree—but who knew that it needed to be made easier?!

BrightScope plans to build public-facing wholesaler pages based on whatever can be found in SEC and FINRA data.

Your firm is probably capable of distributing product data to every new data distribution partner that emerges. But this BrightScope feature raises a question about the readiness of your wholesaler contact data and your ability to take advantage of visibility opportunities on BrightScope and other third-party sites in the future.

If you haven’t already (and my impression is that many firms have not), I’d get your wholesaler information into a database. Clean it up, make sure the go-forward maintenance responsibility is assigned and prep it for distribution to augment whatever files others can pull from the regulators' data feeds.

Another intriguing vision worth learning more about: “FAs [financial advisors] will see data and be able to tie in articles they [wholesalers] write on, say, a specific fund or firm, to be seen by investors.” To date to my knowledge, wholesalers are writing few if any articles and likely none to be seen by investors, but we shall see where that goes.

Ad-targeting capabilities

Ad targeting is mentioned in the MFWire post but not in the BrightScope post. Already a site with some advertising on it, BrightScope plans to leverage its advantage of running a platform of registered users by offering the capability to target specific users as well as viewers of specific pages.

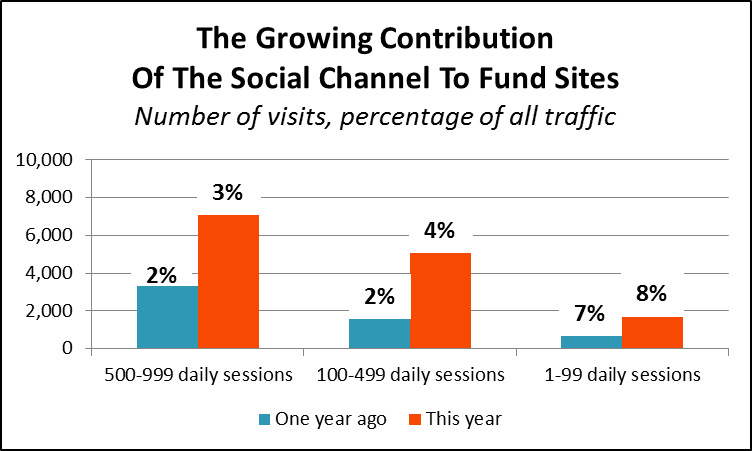

Insights Into Social Financial Literacy

Early in the week, I saw a few mentions of an infographic presenting the highlights of a Transamerica study of social financial literacy.

The infographic embedded on the LinkedIn Marketing Solutions blog presented only the results of LinkedIn users’ (oh, LinkedIn, there you go again, being all LinkedIn-y). Later, I found a Transamerica SlideShare deck dated June 5 presenting the overall results, although not the same kind of data highlighted in the LinkedIn deck.

The first screenshot below is from the overall deck. What I found most interesting: Of all the social networks, Reddit and Twitter users are most likely to pay to meet with a financial advisor.

This second image below is a combination of two datapoints from the LinkedIn deck. As you can see, eight out of 10 LinkedIn users say they won't pay to meet with an advisor, although four out of 10 say they have met with an advisor. Two-thirds of LinkedIn users say it's unlikely they will pay to meet with an advisor. Oh my.

I made an effort to find someone at Transamerica who can provide a narrative on the results but no luck so far. June 19 update: Evidently, I've jumped the gun on this. Transamerica has reached out and said they're about two weeks away from giving this work the formal reveal it deserves. Watch this space—assuming there's more to share, I'll write another post.

Kudos to all of you who prepare infographics to present survey results. Just be sure to include the basics about the survey on the infographic so it can stand on its own. Without knowing the total number of responses, the methodology etc., it’s hard to know what to make of these somewhat alarming findings. The overall deck is embedded below.

Can Social Finance Work?

Executing in financial services can be tricky, nobody needs to tell you that. But you might be interested in following a discussion that’s happening this week about whether social finance can work.

If it can, of course, your job is headed for change. (Last month, 77% of surveyed financial services marketing executives told the 2015 Makovsky Wall Street Reputation Study that they are concerned about losing customers to alternative providers.)

I had mixed reactions to Tuesday’s TechCrunch blog post, “Why Has ‘Social’ Failed In Fintech?” I thought it had value as a round-up, if pessimistic, and the comments showed an encouraging level of interest in the topic.

But a few points in the post didn’t sound right. Example: The statement that “a recent analysis of Facebook Ads by Salesforce.com shows finance ads to have one of the lowest click-through rates at 0.2 percent.” The work is from 2013, and while CTRs on finance ads were not the best, they also were not the worst performers.

Ultimately, I decided against sending a tweet about the post but it continued to weigh on my mind.

Then Howard Lindzon, StockTwits founder and the real deal in fintech, published a response that disagreed with the TechCrunch blogger’s premise. Social has not failed in Fintech, Lindzon wrote in “What Is Taking Social Finance So Long?” It is underway.

However, Lindzon wrote, “The author fails to point out that social finance has been guarded by antiquated rules of FINRA and the SEC, and no other industry that has tried to become more social has faced more regulatory and incumbent pushback.”

This cheered me and I thought it would you, too. Take heart—even the would-be disruptors find your environment challenging. And, also like you, they’re not giving up.